Lab Review 3

Hoang Nguyen

Feb 17, 2017

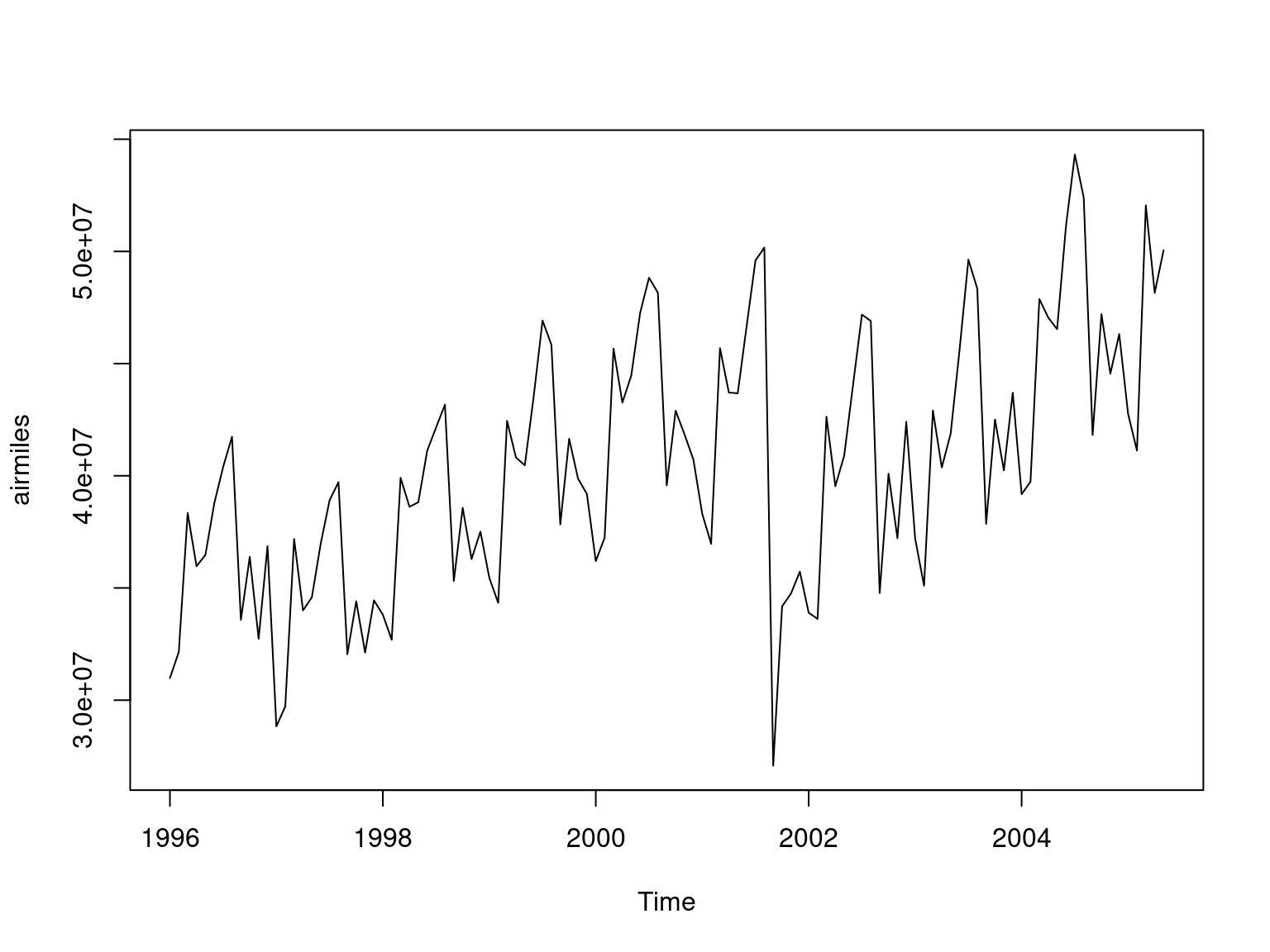

Another example of the Monthly U.S. airline passenger-miles: 01/1996 - 05/2005.

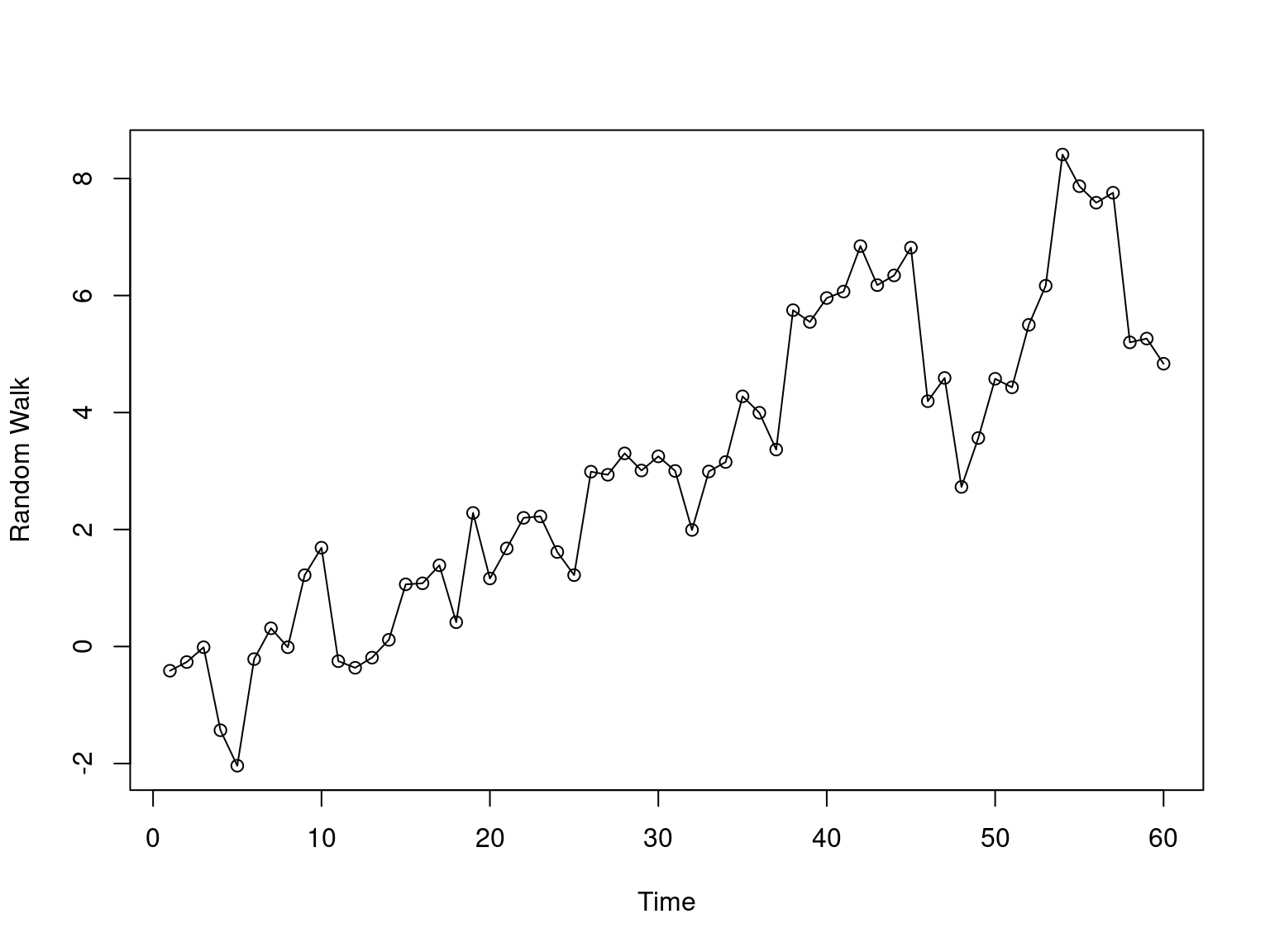

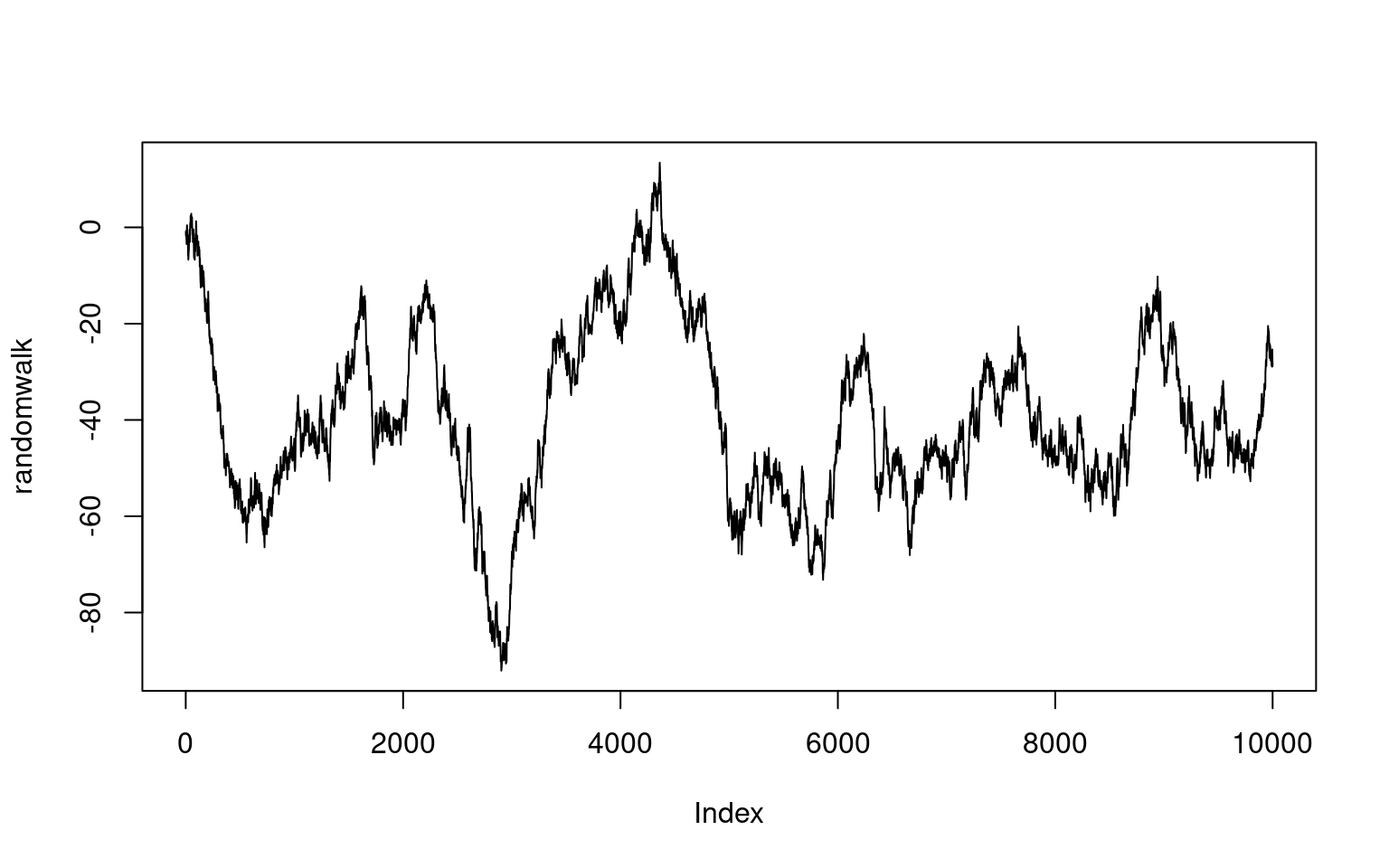

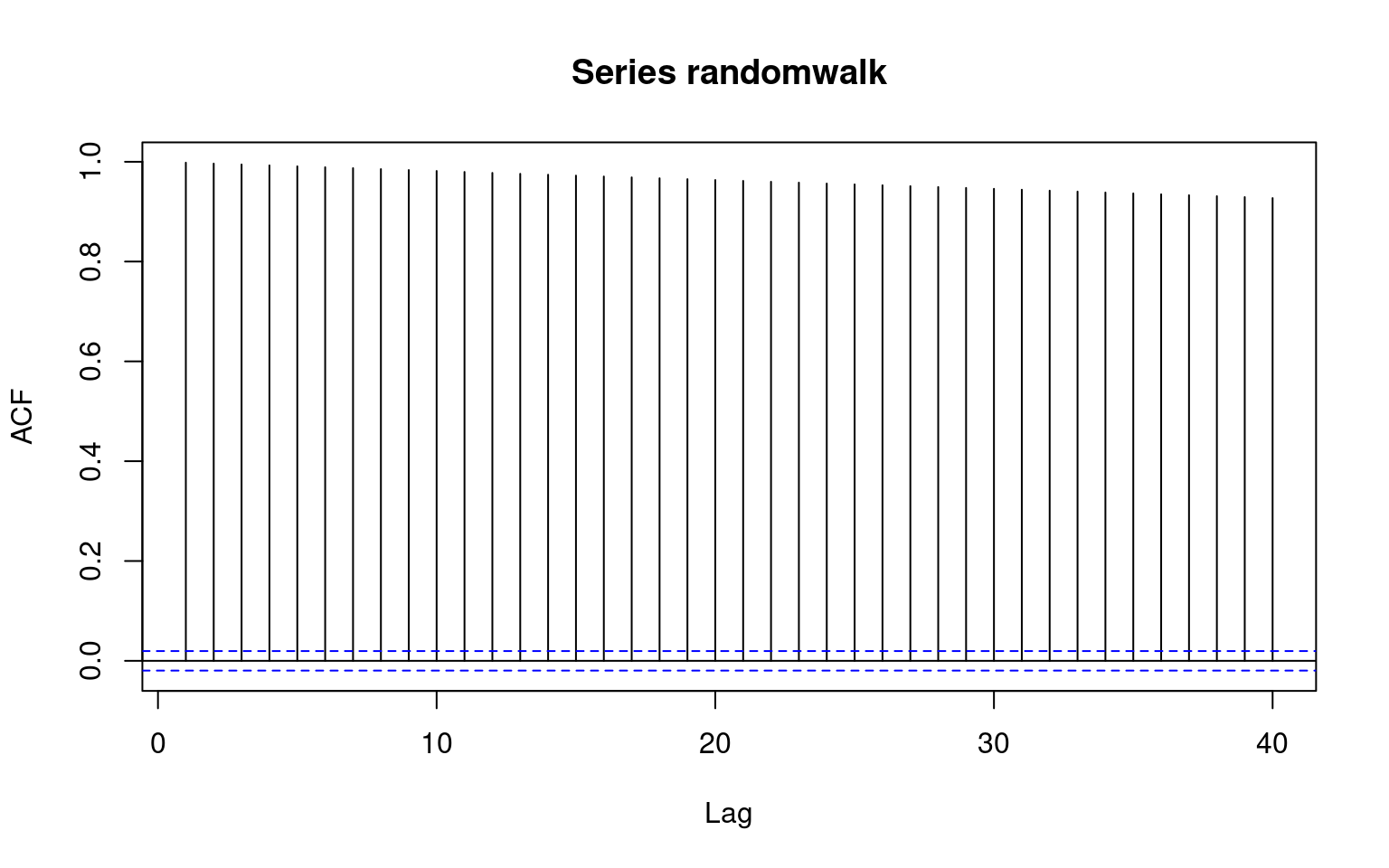

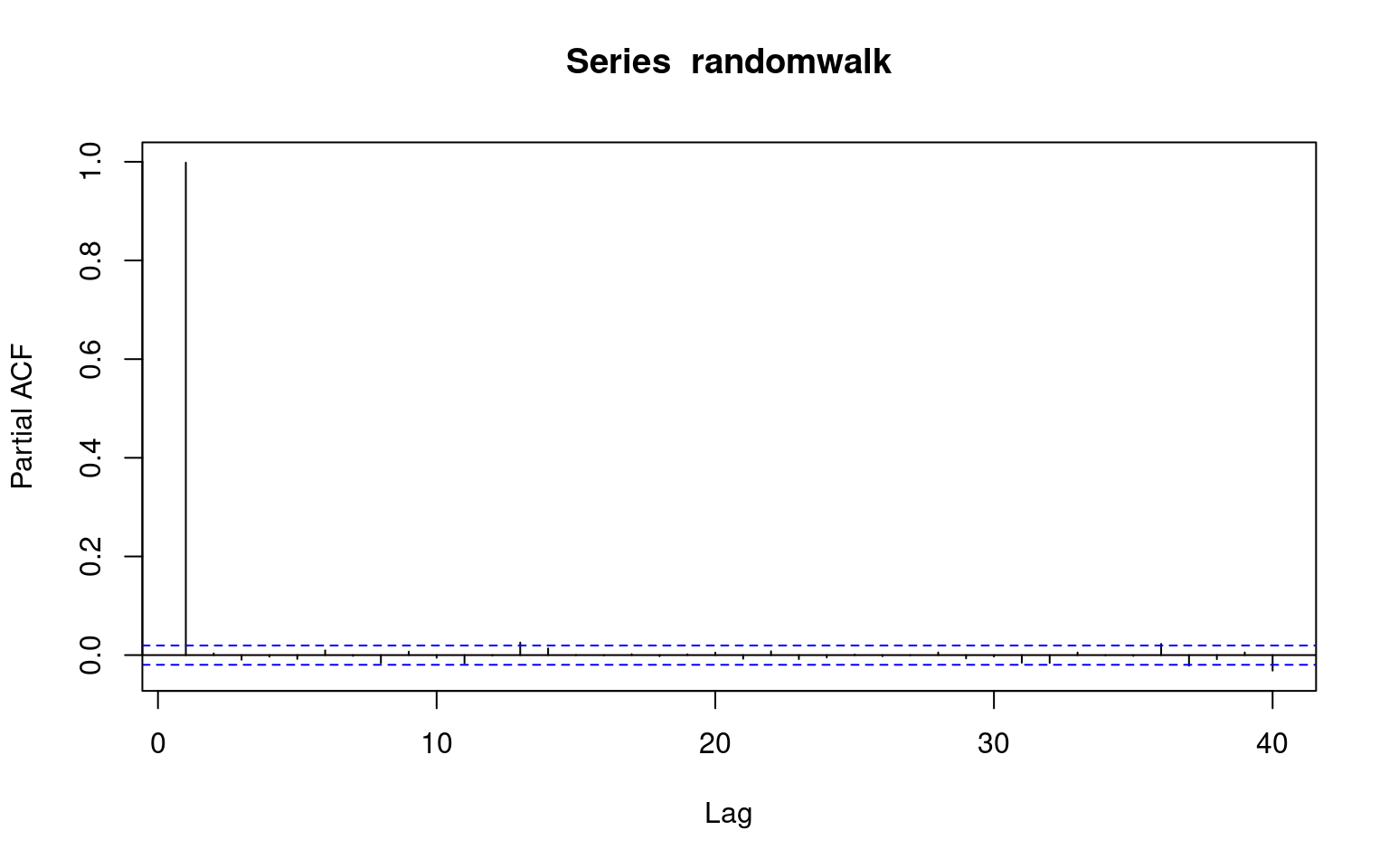

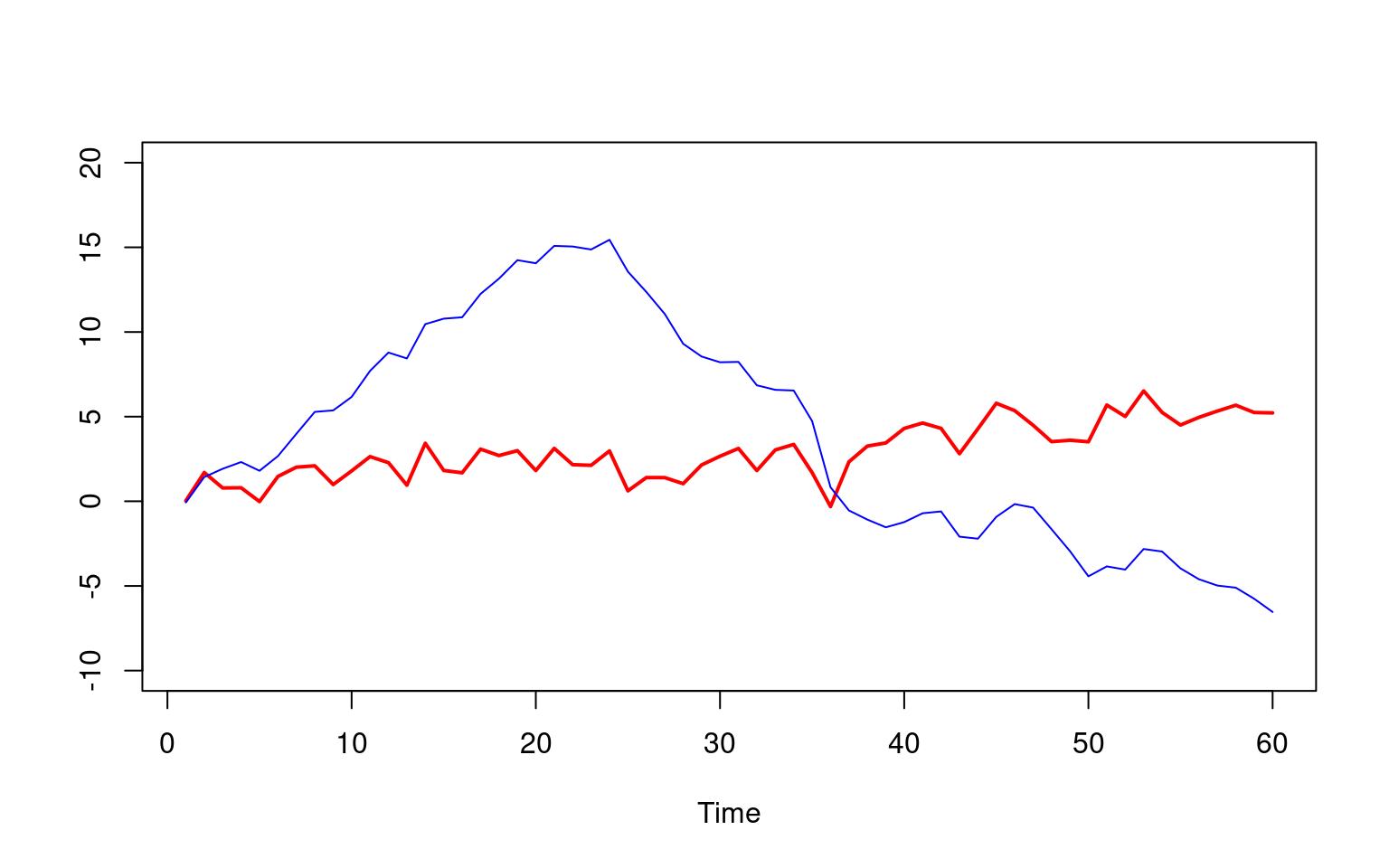

Random walk is stationary?

eps = rnorm(10000)

randomwalk = cumsum(eps)

plot(randomwalk, type = "l")

acf(randomwalk)

pacf(randomwalk)

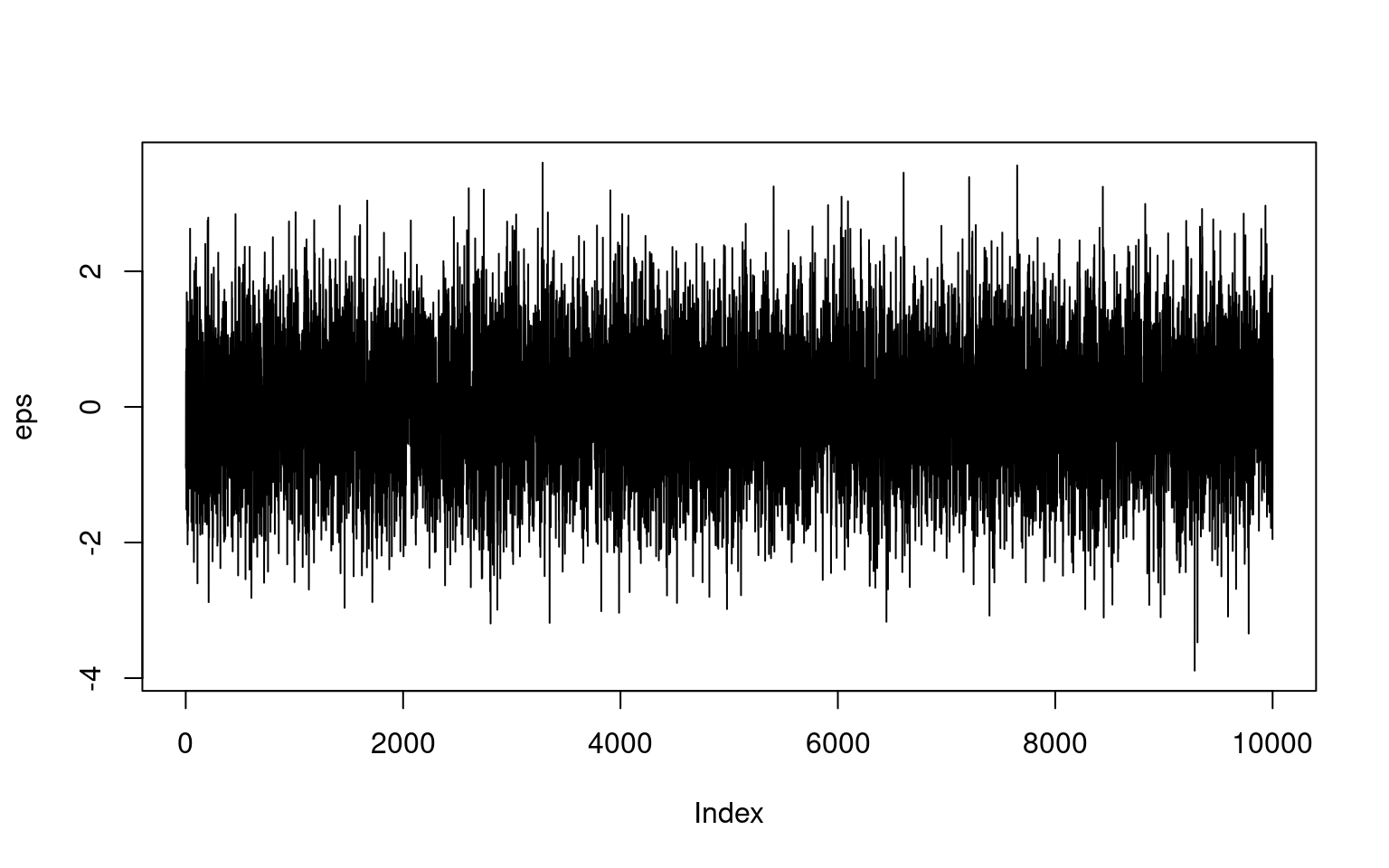

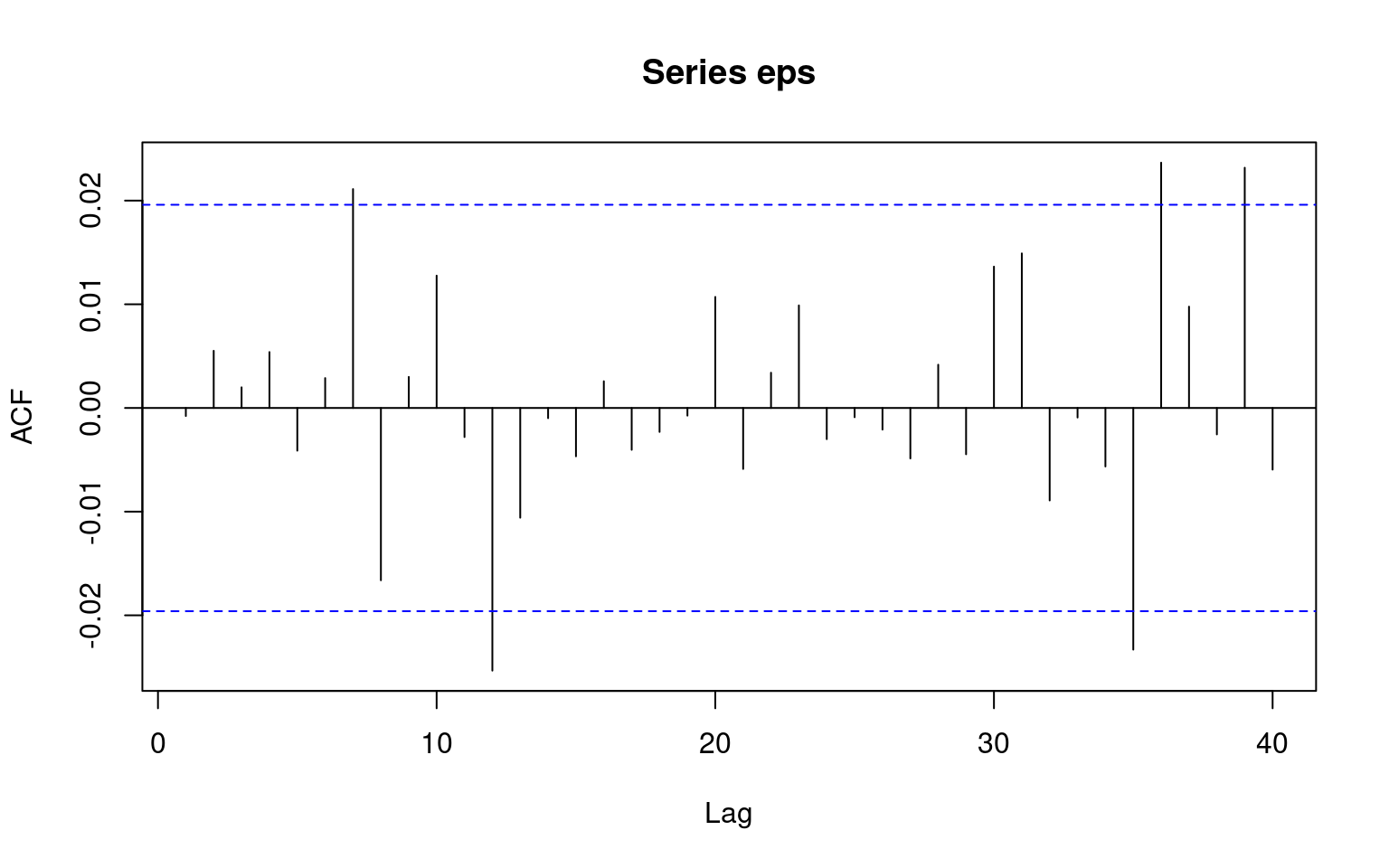

White Noise

plot(eps, type = "l")

acf(eps)

pacf(eps)

Make your guess?

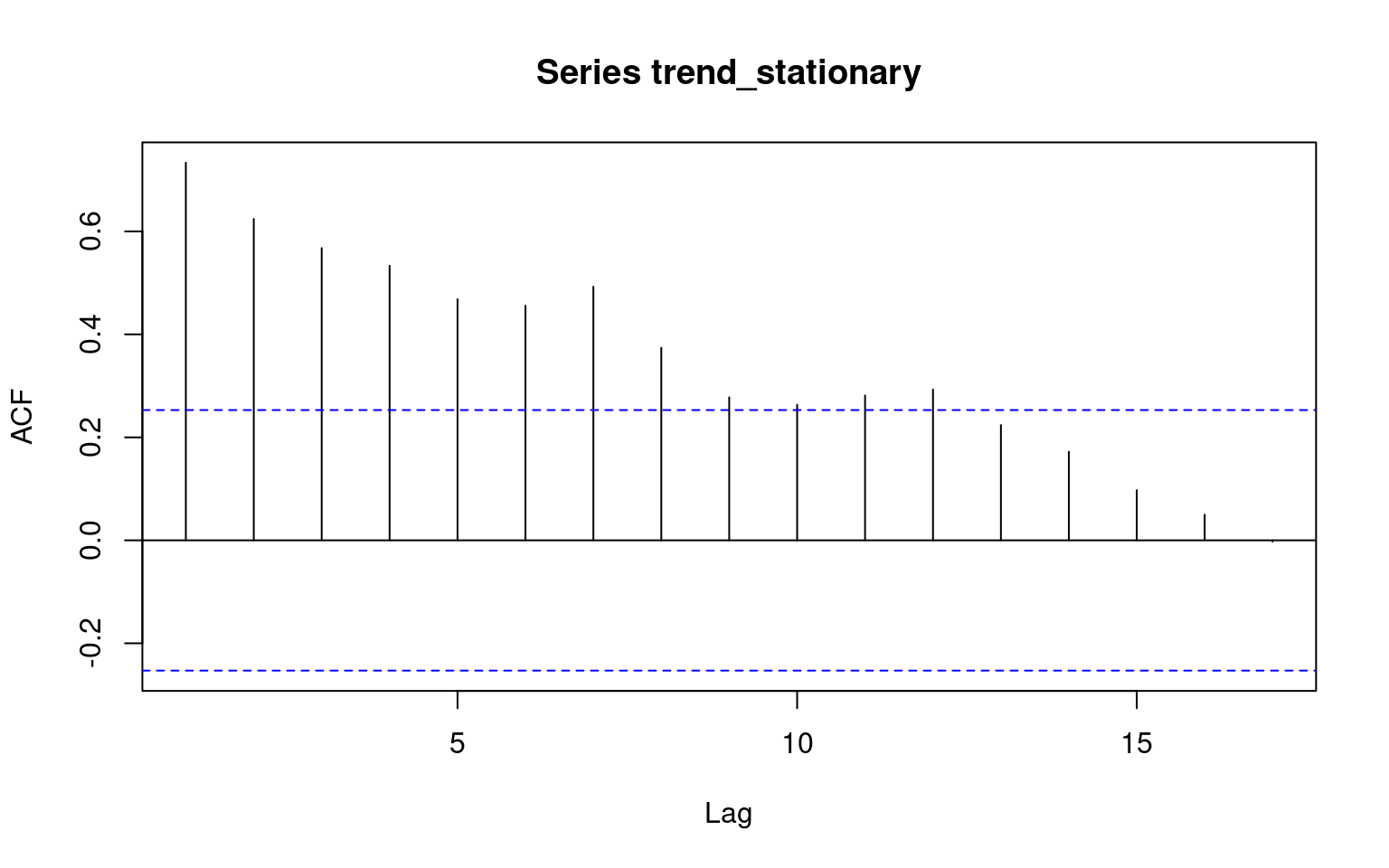

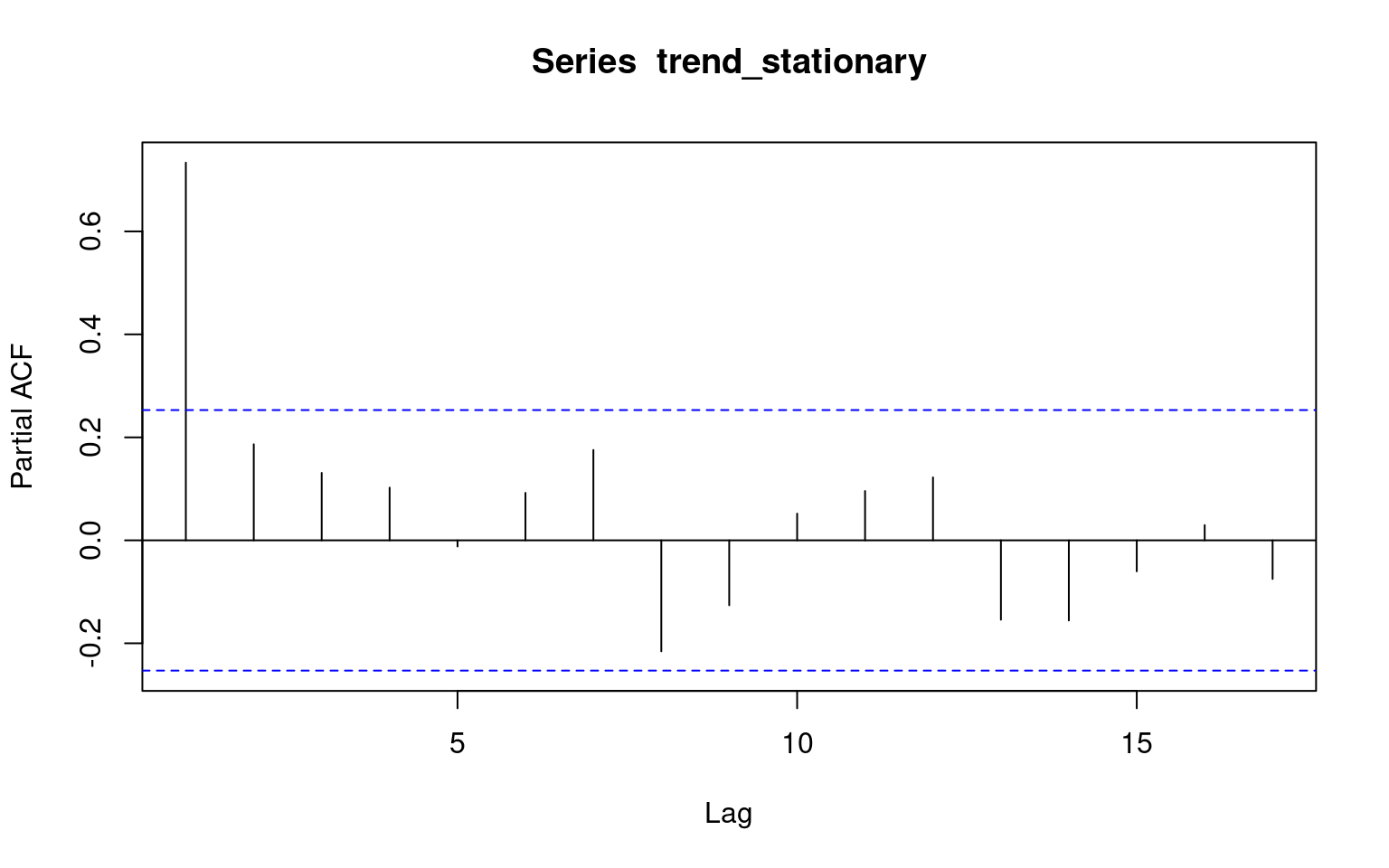

Trend Stationary or Difference Stationary

acf(trend_stationary)

pacf(trend_stationary)

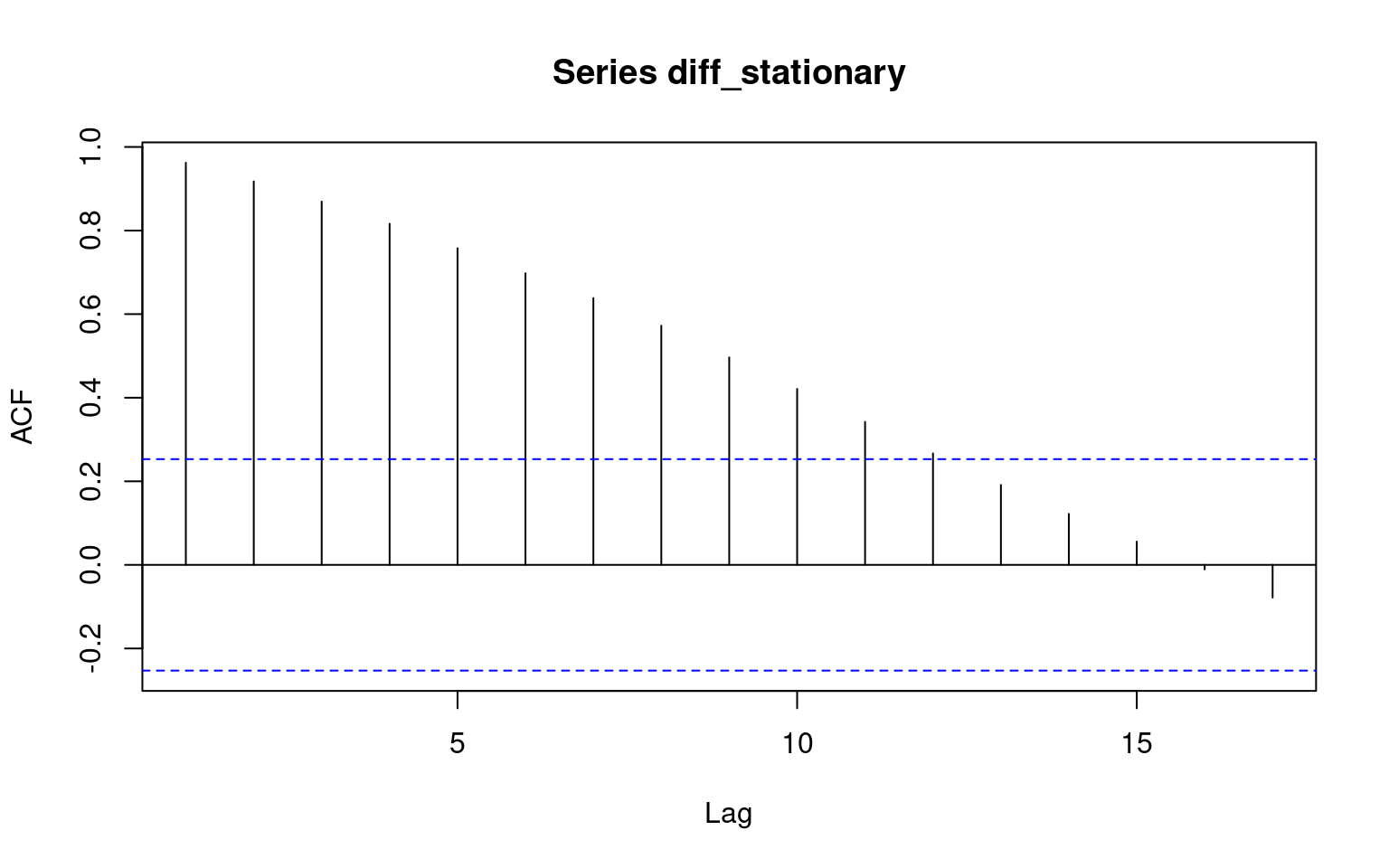

acf(diff_stationary)

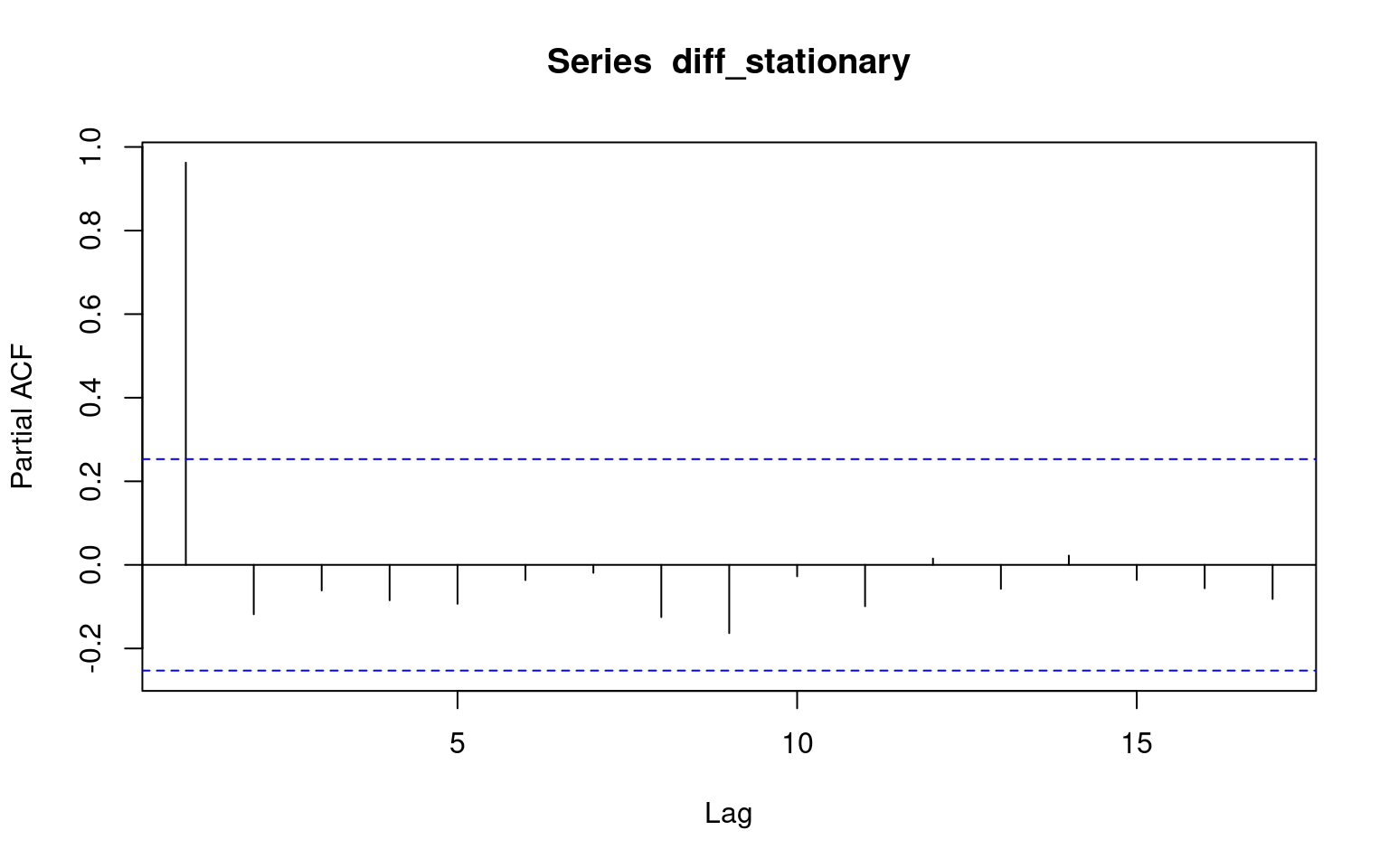

pacf(diff_stationary)